Insights ahead of the 2024 Budget?

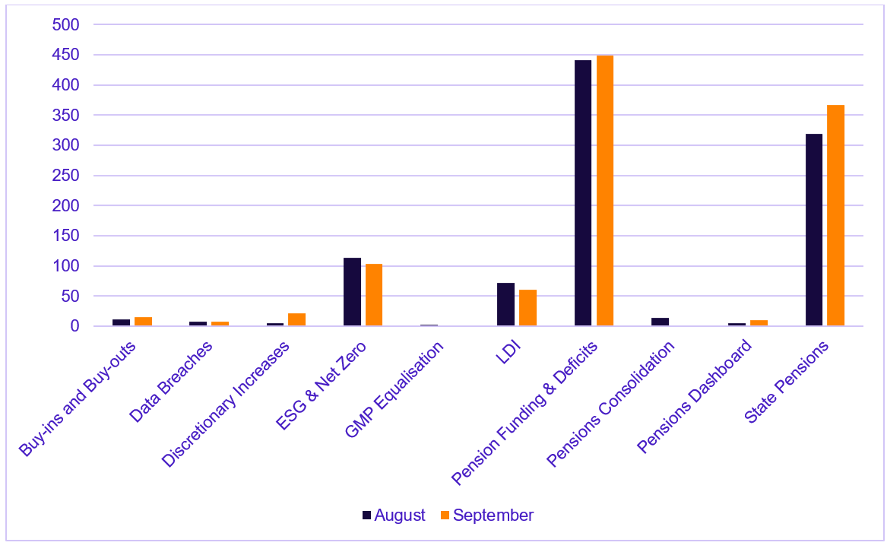

According to SEC Newgate’s analytics Pensions Funding and Deficit remains the leading theme this month with 452 stories, followed by State and Pensions (source: Brandwatch). The most notable pensions announcement is the new government’s Pension Review which is seen as the key area of finance by the government to boost investment in the UK and achieve its key mission of ‘kickstarting economic growth’. There has a been a lot of discussions around how the government will achieve its aims, with many industry commentators suggesting that the government will need to offer targeted fiscal incentives to make UK growth assets more attractive. More will follow in the comings weeks and months as await responses to the consolation to the first stage of the Pensions Investment Review.

In recent months, pension schemes have been strongly encouraged to invest more in UK capital. In September, pension schemes reached an all-time low in their allocations to British stocks, highlighting a significant decline in domestic equity investments. UK pensions hold just 4.4% of their assets in domestic equities, which is far below the global average. This shift has been influenced by regulatory changes pushing schemes toward bonds as they de-risk. Politicians, including Chancellor Rachel Reeves, are exploring ways to boost investment in UK assets by pension schemes, potentially consolidating funds to a "Canadian-style" model. For pension schemes, this means potential regulatory shifts that could push more investment in British markets.

Then we have the upcoming Budget. It is difficult to ignore, the speculations and rumours in the media. With potential reforms including changes to pension tax relief (flat 33% rate to benefit lower earners), changes to the tax-free lump sum limit (might be reduced from £268,275 to £100,000), potentially the government might impose inheritance tax on pensions and apply National Insurance to employer contributions. The freeze on the personal allowance could lead to parts of the state pension being taxed by 2028. This has resulted in a “stampede” of withdrawals from pension scheme ahead of the Budget as pension savers are panicking on the potential implications. However, these changes are speculative and not yet confirmed.

Such potential reforms could create significant challenges. Reducing tax relief or imposing additional taxes on employer contributions could discourage saving, particularly for higher earners, which may force pension schemes to adjust their investment strategies if tax incentives change, particularly those with DC schemes that rely on member contributions. DB schemes could also face pressure if changes to tax-free lump sums affect public sector workers, potentially requiring increased employer contributions to offset the impact.

However, as there still seems to be inequity in pension tax relief, highlighting that higher earners receive a disproportionate amount of relief despite paying most of the income tax. It proposes reforms, including eliminating the 25% tax-free pension lump sum and taxing inherited pensions, which could raise significant revenue. These changes would focus on taxing pensions at the withdrawal stage rather than contributions, encouraging longer working lives and preventing distortions in the tax system.

The proposed pension tax reforms would significantly alter the landscape for retirement planning. These changes could reduce the current tax advantages of drawing down pension benefits, potentially leading to a shift in behaviour, with individuals working longer to achieve desired retirement incomes. Additionally, the focus on taxing withdrawals rather than contributions could influence savings strategies and require pension schemes to adapt their structures to accommodate new tax burdens and ensure adequate retirement benefits for members.

Additionally, the state pension is set to increase by £460 a year in April 2025, with the full new flat-rate state pension rising to £230.05 per week, thanks to a 4% wage growth under the "triple lock" system. This system ensures the state pension increases annually by the highest of wage growth, inflation, or 2.5%. The pension age is gradually increasing, potentially reaching 68 by 2046. Also, changes to pension credit and the winter fuel payment will affect pensioners' financial support, with the latter being cut for those not on means-tested benefits.

These updates highlight the growing fiscal pressure on the state pension system as it becomes increasingly costly for the government. The rising state pension age reflects the need to balance longevity and affordability, and this emphasises a shift towards targeting support to those most in need, while broader tax reforms will affect pensioners differently based on their income brackets.

Total mentions by topic (August - September)

- Pensions funding and deficit saw the greatest number of mentions between August and September with 452 stories, followed by State Pensions with 367 stories.

Examples of Pensions funding and deficit mentions this month

- @PaulLewisMoney - Household Support Fund extended so pensioners who feared losing Winter Fuel Payment and pled poverty to DWP for pension credit but rejected (£220/week too much in some cases) can now plead poverty with local council officials and hope they’re more flexible. Next stop the Parish!

- @CarbonBubble -"The problem with models that estimate climate risk for pension funds is that they are reviewed by economist but not by #climate scientists." @CampanaleMark at #ClimateFinance Day. #ClimateWeekNYC

- @CarbonBubble - Our Founder @CampanaleMark raises the point that it may take losing half the buildings in their real estate portfolio for pension funds to take notice of the risks caused by #climatechange. #ClimateFinance Day #climateweek2024 #ClimateWeekNYC

What to read next

Browse below for the latest news, insights and thought leadership from our team of experts

Local Elections 2026: Your guide.

Scotland: The Battle for Holyrood

No decision yet for Sussex and Brighton & Hove

Reed update provides more clarity on future for local government

Engaging Topics: What about the value of my home?

What’s changing for planning committees and why it matters

Pension Talks Interview: Jane Beverley, Senior Director, Law Debenture

Pensions and Politics: a risky mix?