Will 2021 continue the rising trend of private fundings?

The IPO market has been very buoyant since the start of 2021, with a high number of companies choosing to come to the market as the country emerges out of the pandemic. But how does that compare to the numbers of private companies hoping to raise money through private fundings? Many have argued that the lack of private funding for start-ups and high-growth businesses has been a real concern in the UK over many years.

However, those companies with the right story to tell, showing high growth potential, be they at a venture capital or growth capital stage are receiving a lot of interest from numerous sources of private capital. Data from Beauhurst suggests that the boom experienced in the public market is being replicated across private markets.

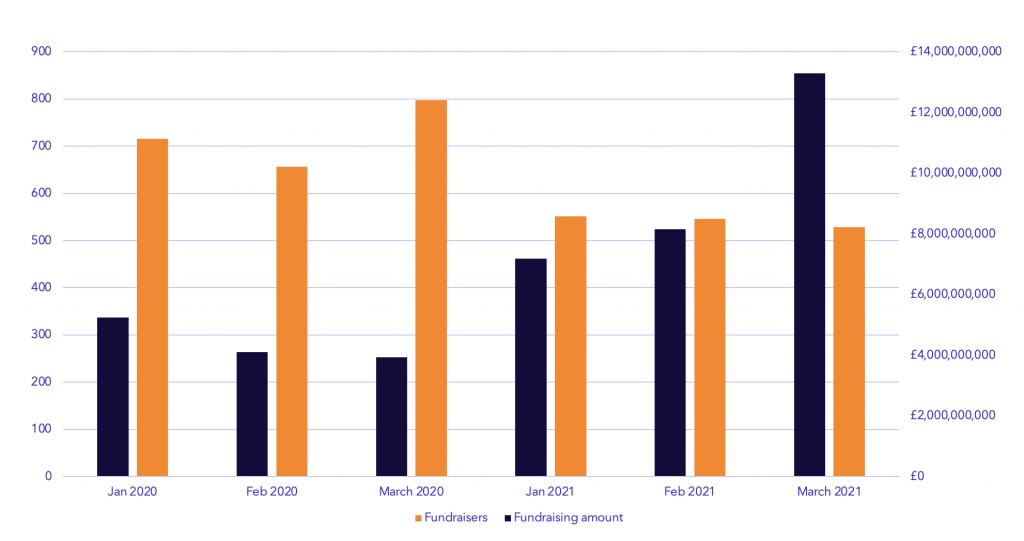

In Q1 2020, 2,155 companies, received private funding in the UK. January 2020 saw 716 fundraises worth £5.25bn, whilst February had 656 deals amounting to £4.10bn and March 798 raises totaling £3.93bn. This suggests that investors were perhaps slightly concerned by the potential impact the pandemic might have on businesses and as a result, invested in more companies but with smaller amounts raised.

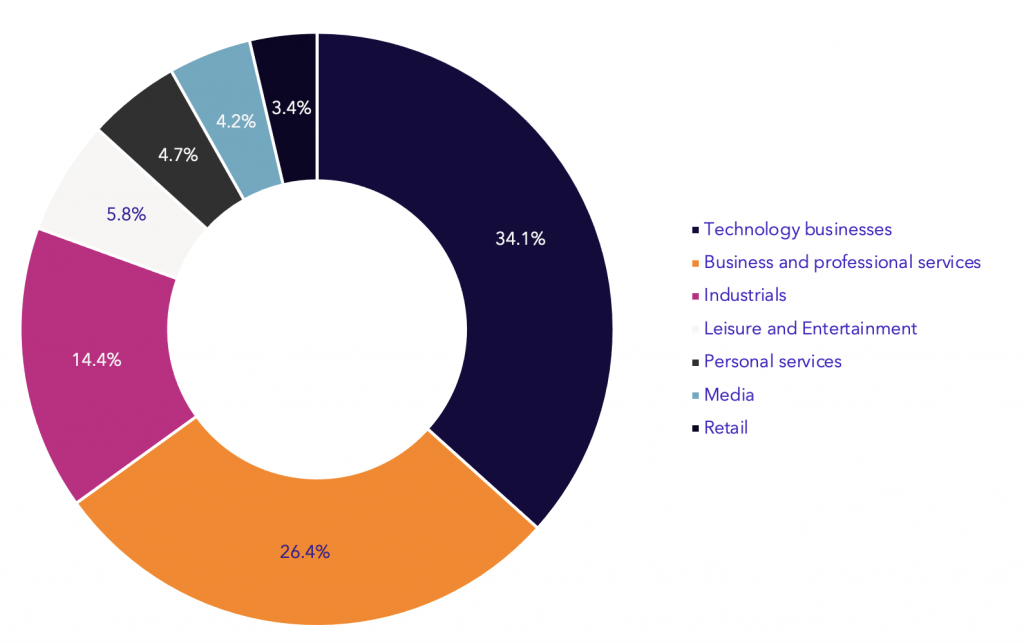

The Beauhurst data also suggests there was a real appetite for start-ups and high-growth businesses in the technology space. 34.1% of Q1 2020 fundraisings were for Technology businesses. Business and professional services and industrial sectors also saw high investments representing 26.4% and 14.4% respectively of total investments. Leisure and Entertainment represented 5.8% of the chart, Personal services 4.7%, Media, 4.2% and finally retail at 3.4% made up the total of UK private fundraisings. Most of the funds came from private equity and venture capital funds, followed by corporate and angel networks.

How does this compare to Q1 2021? The pandemic and numerous lockdowns in the UK have not dampened investor appetite for private funding. This quarter, 1,615 companies received private funding in the UK. That is slightly less than Q1 2021, however those companies received higher levels of private funding. January 2021 saw 551 fundraisers worth £7.19bn (Q12020: £5.25bn), February fund raisings nearly doubled in investments to £8.15bn (Q1 2020: £4.10bn) from 546 fundraisers, whilst March 2021 investments were up 238.42% or £13.3bn (Q1 2020: £3.93bn) from 528 fundraisers.

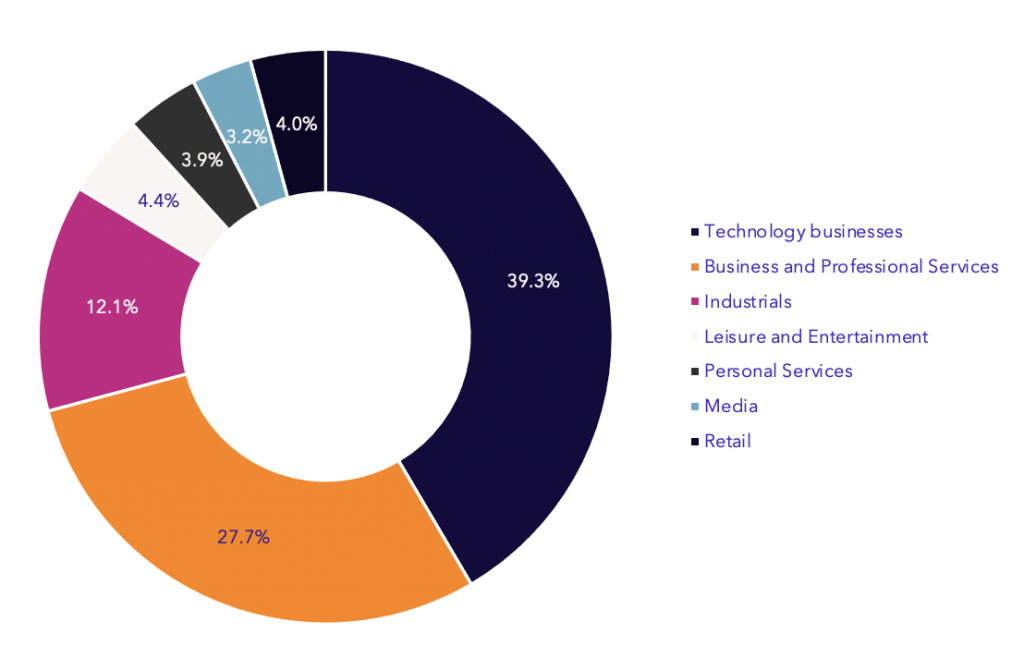

In terms of sectors, Technology is still the preferred sector, representing 39.3% of investments. Business and Professional Services (27.7%) and Industrials (12.1%) also continue to attract private funding interest. Leisure and Entertainment (4.4%) Personal Services (3.9%) and the Media (3.2%) sectors fared less well than Q1 2020, whilst retail nudged up slightly represent 4% of total investments. As before, private equity and venture capital were the biggest players this quarter, followed by corporates and angel networks. Central government funding also increased considerably this quarter, perhaps linked to the Future Fund launched by the Government in April 2020.

The findings reveal that private companies are still getting high levels of interest and support. There are significant pools of private capital that are always looking for high growth businesses to invest in. But before any round of funding begins, a valuation of the company needs to be conducted. Valuations are derived from many different factors, including management, proven track record, market size and risk. These factors impact the types of investors likely to get involved and the reasons why the company may be seeking new capital. The biggest challenge for investors and companies alike is being able to find each other away from the public markets. From a communications stand-point, it is extremely important for private companies to start developing those key messages to ensure they raise their profile and get their story to the investing community so they can drive the right valuation. Those who manage that best, regardless of the sectors in which they operate, are most likely to emerge as the winners, with higher valuations.

What to read next

Browse below for the latest news, insights and thought leadership from our team of experts

Pensions Talks Interview: Donald Fleming, Professional Trustee, Pi Partnership

Pensions in play: Autumn Budget, Reform pressure, and political shifts

Charlie Kirk, “outrageous things”, and viral politics

Markets run on stories and Europe’s IPO market needs a bestseller

A new era for higher education: London’s first "super-university" signals bold future

“Power On” - shining a light on Climate Week NYC

Reform has its Roundhead moment in Warwickshire

Forget SEO, it’s time to think about GEO