Wealth, moats and the levelling down agenda

Is a UK wealth tax on the way?

Credit Suisse’s Global Wealth Report 2021 certainly gives the Treasury something to think about. Despite historic falls in GDP, UK wealth has risen in the past year. Mean wealth per adult has grown $20,200; median wealth has grown $8,100[1]. This equates to 7.5% and 6.6% respectively.

Such growth is remarkable in the current economic distress; wealth normally tracks GDP growth.

Much comes from the Bank of England slashing interest rates and buying bonds. It also reflects the UK’s strict lockdown; with nowhere to go, Britons have saved voraciously. The Q2 2020 savings rate was 26.5% the highest in history. The spending that would have driven GDP has grown wealth instead.

The wealth gap

Wealth distribution is notoriously unequal. The UK GINI index – which measures inequality in distribution - was 71.7 for wealth in 2020 (the index runs from 0 – 100, with 100 being the most unequal). By contrast the income GINI was 34.6 in 2020[2].

Globally the pandemic increase wealth inequality at a higher rate than any year this century; the share of wealth of the global top 10% increased by 0.9% and the top 1% by 1.1%. The global wealth GINI increased by 0.6.

This is reflected in the UK. The wealthiest have the largest asset bases and are saving more – the most affluent areas saved £12 for each £1 saved in the poorest areas, according to think tank Centre for Cities.

There is a strong North South divide, with Southern cities radically reducing their spending during the pandemic relative to Northern cities and saving more.

Time for tax?

This provides a challenge for the Government. Its stated agenda is to “level up” less affluent groups and regions. But public finances have deteriorated significantly due to the pandemic. To balance the books, tax increases are required.

With manifesto restrictions on raising income tax, the government is reported to be eyeing wealth taxes. Already there are signs of action. In this weekend press, talk emerged of reducing the lifetime pensions allowance to £800,000. This effectively taxes pensions wealth, with the threshold halved from £1.8m in just a decade.

Proposals have been floated for a “one off” wealth tax of 1% on individuals with over £1m in net assets which could raise £260bn. The controversial Mansion tax, long ago rejected, is being mentioned again.

But wealth taxes are unpopular. The most famous British wealth tax, the window tax of 1,696 created swathes of dark, windowless buildings.

A mansion tax may disproportionately impact pensioners – a critical Tory voting cohort - who are asset rich but income poor. A wholesale wealth tax could spur the wealthiest to move their assets (or themselves) abroad.

Disparities keep growing.

It is not clear that greater taxation will drive greater wealth or regional equality.

In the past 20 years the Government has raised income tax, reduced pensions annual contributions and lifetime allowances, increased stamp duty, reduced property tax relief and tinkered with CGT. The tax to GDP ratio in the UK in 2019 was 33%, up from 31.1% in 2003. Despite this, the GINI wealth coefficient has got worse, ticking up from 70.7 in 2000 to 71.7 in 2020.

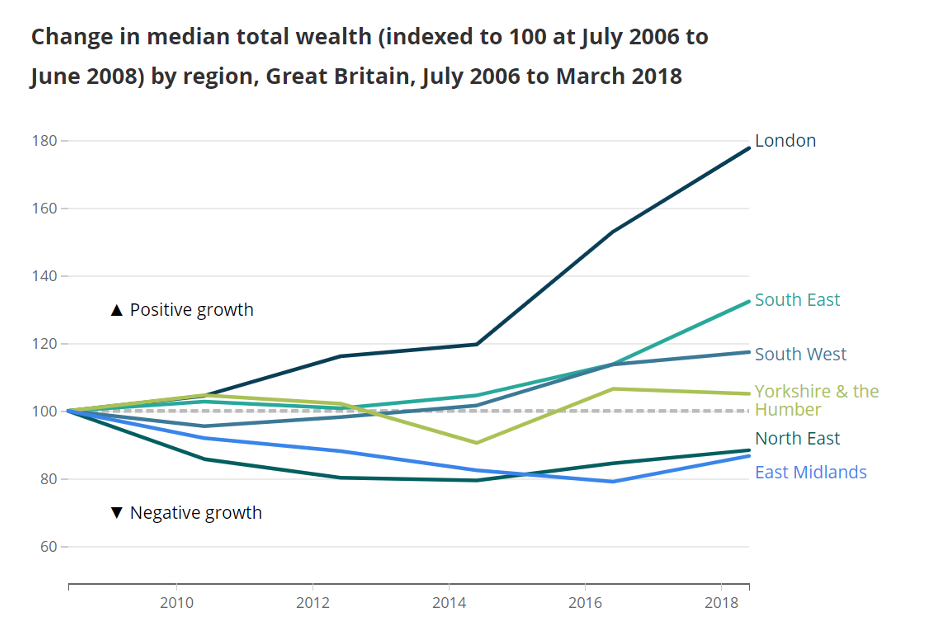

On a net basis, London and the South-East contribute 93.6% of the surplus fiscal balance in the UK[3]; the largest fiscal deficits are in the North and Midlands. Despite this, the median wealth growth of London and South-East keeps outpacing other regions.

Quite simply, fiscal distribution has not yet led to greater equality.

Can the gap be closed?

The reasons for wealth inequality are complex. History has shown that fiscal transfers can alleviate short term inequality but not longer-term structural issues.

The concept of economic moats is important for generating wealth; moats are factors that help a company, region or economy to maintain an advantage against competitors. The City of London is a formidable moat; the concentration of talent, ancillary professional services and infrastructure has maintained its pre-eminence despite the massive disruption of the global financial crisis and Brexit.

There is evidence that moats exist within society, allowing the wealthiest to pass the education, confidence and wealth for future generations to succeed.

But it is hard to see where moats will exist in the most deprived areas and groups of the UK.

Although Brexit may provide some protection against jobs and trade from Europe, global competition is strengthening. Remote working proves jobs can be done anywhere in the world. Covid 19 may have changed the nature of globalisation, but not the pace of it.

Without sustainable moats, any distribution of wealth will be transient.

Levelling up or down?

There is a risk that in trying to level up regions, others are levelled down. Despite the increase in UK wealth in the past year, it pales compared to other countries.

Mean wealth in the UK may have increased $20,200, but Belgium’s increased $54,030 and Australia’s $65,700. It is not just the wealthiest who are benefiting– median wealth increased $35,300 in Belgium and $32,280 in Australia, as opposed to $8,100 in the UK.

The growth in the UK rich is not keeping pace with other countries. 1.7% of the UK population were millionaires in 2000; today that figure is 4.7%. 0.8% of the Australian population were millionaires in 2000; today it is 9.4%. France’s was 0.9% and is now 4.9%.

The UK’s wealth inequality is not remarkably worse than other countries; that is not to say it is fair nor that we should try to solve it. What is clear is that past actions have both failed to close inequalities and keep pace with the greater wealth boom in other countries.

A wealth tax may seem an easy panacea. It would be popular amongst those who do not have to pay it. It would be paid by relatively few.

On its own, it will not provide the structural reform required. It risks providing a simple solution to a complex problem and veiling it in populism. Most importantly, it may not close the wealth gap within the UK, while potentially widening the gap between the UK and global leaders.

[1] Mean measures average adult wealth. i.e., the total wealth of a country divided by the number of adults. Median measures the midpoint of the distribution of wealth. Median is often considered a better representation of the typical wealth of individuals in a country than the mean; this is because mean figures can be skewed upwards by a few very wealthy individuals.

[2] Source: Office for National Statistics

[3] Fiscal surplus (or deficit) is the difference between the amount paid in tax to the Government and the amount of money spent by the Government in a region.

What to read next

Browse below for the latest news, insights and thought leadership from our team of experts

Back on the energy rollercoaster

It's time to stop demonising business

Is the UK ready for war?

When platforms become liable

Engaging with the next frontier of sustainability

Four reasons London still reigns supreme for capital markets days… And it’s not just nostalgia

Why renewables now sit at the heart of global security

Energy prices in the spotlight as Reeves addresses MPs